By RIA Team

Publication Date: 2025-11-20 09:25:00

Fears are spreading on social media that some AI players are on the verge of default. The proof, some say, is in the Bloomberg charts below, which show Oracle and CoreWeave’s growing CDS spreads. Before we delve deeper into the CDS markets’ warnings about Oracle and CoreWeave, let’s first explain what CDS is.

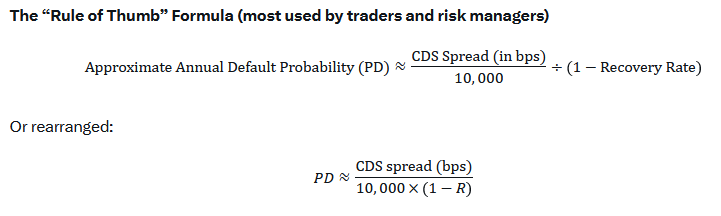

CDS stands for credit default swaps. These are derivative contracts in which one party, the buyer of the default protection, pays a quarterly fee, expressed in basis points. In return, the counterparty or security provider assures that the buyer will receive the face value for his bonds in the event of default. CDS spreads, or the cost of default insurance, provide the market with an easy way to quantify the implied probability of market default. Although simplified, here is the math to calculate default risk:

Essentially, the formula divides the cost of insurance by the face value of the bond minus the repayment rate. The recovery rate represents what bondholders…

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg?ssl=1 "Should You Buy Oracle Stock Ahead of TikTok USA’s New Spinoff?")