Stock Before Q4 Earnings: To Buy or Not to Buy?")

Nutanix (NTNX – Free Report) is set to release fiscal fourth-quarter 2024 results on Aug 28.

For the fourth quarter of fiscal 2024, Nutanix expects revenues in the range of $530 million to $540 million. The Zacks Consensus Estimate for the same is currently pegged at $537.12 million, suggesting 8.7% growth from the year-ago period.

The Zacks Consensus Estimate for earnings has remained unchanged at 19 cents per share over the past 30 days, indicating a decline of 20.8% from the year-ago period.

Image Source: Zacks Investment Research

In the last reported quarter, Nutanix delivered an earnings surprise of 64.71%. Markedly, the company’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average being 63.48%.

Earnings Whispers

Our proven model does not conclusively predict an earnings beat for Nutanix this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Nutanix has an Earnings ESP of 0.00% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors to Consider

Nutanix’s fourth quarter of fiscal 2024 performance is expected to have benefited from the solid adoption of its hybrid cloud solutions and an expanding clientele. Nutanix continues to witness strong growth in core hyper-converged infrastructure (HCI) software and the solid adoption of its hybrid multi-cloud solutions across Fortune 100 and Global 2000 companies.

Strong demand for Nutanix products and a high customer satisfaction rate are helping the company expand its customer base. The company’s built-in hypervisor has been gaining significant traction as customers continue to select it as a low-cost alternative to other vendor offerings. Its cloud-based deployment strategy is a differentiator. NTNX’s Xi Cloud Services is expected to challenge AWS, Microsoft Azure and Google Cloud in the infrastructure-as-a-service market.

Nutanix’s growing recurring revenue stream reflects customer loyalty to its solution portfolio, which improves the visibility of its revenue growth trajectory.

During third-quarter fiscal 2024, the company added 490 new customers, bringing the total client number to 25,860. Further, the company’s transition to software-only sales is expected to significantly boost gross margin. In the fiscal third quarter, non-GAAP gross margin expanded 250 basis points year over year to 86.5%.

For the fourth quarter of fiscal 2024, Nutanix expects Annual Contract Value billings between $295 million and $305 million.

Price Performance & Valuation

Nutanix has seen its stock gain 10.3% year to date, underperforming the Zacks Computer and Technology sector’s return of 22.3%. Nutanix operates in a fiercely competitive market dominated by established players and cloud giants, which could put pressure on Nutanix’s market share and margins in the near term. Key rivals include VMware, Dell Technologies (DELL – Free Report) and Hewlett Packard Enterprise (HPE – Free Report) , all of which offer similar solutions for hybrid and multi-cloud environments. Additionally, public cloud giants like Amazon Web Services, Microsoft (MSFT – Free Report) Azure and Google Cloud Platform pose indirect competition as enterprises increasingly shift workloads to the cloud.

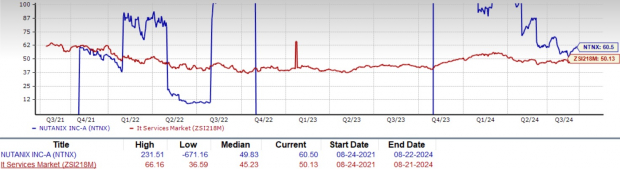

Valuation-wise, the company’s three-year trailing 12-month EV/EBITDA ratio of 60.5 is ahead of the Zacks Computers – IT Services industry average of 50.13. This premium valuation is partly justified by Nutanix’s strong revenue growth and successful transition to a subscription-based model. However, it also leaves the stock vulnerable to market volatility and any perceived slowdown in the company’s expansion.

NTNX’s 3-Year EV/EBITDA TTM Ratio Depicts Stretched Valuation

Image Source: Zacks Investment Research

Investment Considerations: Balancing Risk and Reward

Nutanix presents a compelling investment opportunity in the hybrid cloud infrastructure market. The company’s software-defined HCI simplifies data center operations, offering scalability and cost-efficiency. Nutanix’s transition to a subscription-based model is enhancing recurring revenues and customer retention. Its expanding product portfolio, including database management and desktop-as-a-service solutions, diversifies revenue streams. Strong partnerships with major cloud providers and a growing customer base across various industries demonstrate market validation. While facing competition from established players, Nutanix’s innovative approach and focus on simplifying complex IT environments position it well for long-term growth in the evolving cloud computing landscape.

Conclusion

For those considering how to play Nutanix stock in the fourth quarter of fiscal 2024, a nuanced approach is warranted. Despite the competitive landscape, Nutanix’s strong position in the growing hybrid cloud market and expanding customer base suggest that it may be premature to abandon the ship. New investors should wait for a better entry point for Nutanix, which currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Article Source

https://www.zacks.com/stock/news/2326368/nutanix-ntnx-stock-before-q4-earnings-to-buy-or-not-to-buy